DExit: So You Want to Leave Delaware? What To Consider Beyond the Legalese

Leaving Delaware is a decision that must be carefully considered over a period of time. Boards must candidly assess the potential advantages and risks of reincorporating to determine what is best for their shareholders. These considerations change notably for companies with specific circumstances (for example, those with large or controlling shareholders).

Of course, the top priority in this assessment should be the legal framework that will be applied to the Company in each state. With that said, there are important non-legal factors to consider when assessing the feasibility and appeal of reincorporating:

- Reincorporation will draw attention from investors and other stakeholders;

- Reincorporation requires shareholder approval; and

- Reincorporation can impact the relationship between a Company and its shareholders.

As a result, Boards looking to reincorporate should:

- Have a strong understanding of not only how their shareholders view reincorporation, but also the current shareholder rights profile, the Board, and the Company’s current reputation with its shareholders. These factors all interplay when shareholders assess a reincorporation proposal.

- Clearly and persuasively articulate the benefit shareholders will receive from reincorporation – both in the proxy statement and in engagements leading up to the shareholder vote.

The Shareholder View on Reincorporation: Frameworks Still Being Established

While DExit proposals have increased over the past two years, this is still a novel topic for stewardship teams and proxy advisors to digest. When stewardship teams grapple with a new proposal or emerging trend, they often take a case-by-case approach at first, and then as the trend persists and there is more data to analyze, they start to develop a voting framework.

Take, for example, the existence of “one-off awards” or retentive awards in executive compensation. As these went from extremely rare prior to the COVID-19 pandemic to increasingly popular during and afterwards, many stewardship teams and proxy advisors built out established frameworks for how to assess these awards. While stewardship did assess and vote on these awards as part of Say on Pay packages previously, these published frameworks now help Boards understand how to design retentive awards in a way that is less likely to result in shareholder dissent. It just took time for investor “frameworks” or “guidelines” to develop. We expect that voting policies on DExit may evolve at a similar pace.

For now, investors’ and proxy advisors’ views generally approach reincorporation on a case-by-case basis, assessing the rationale for reincorporating (often looking for more than simply ‘less litigation’), economic benefit, change in shareholders’ rights, and a company’s broader governance profile.

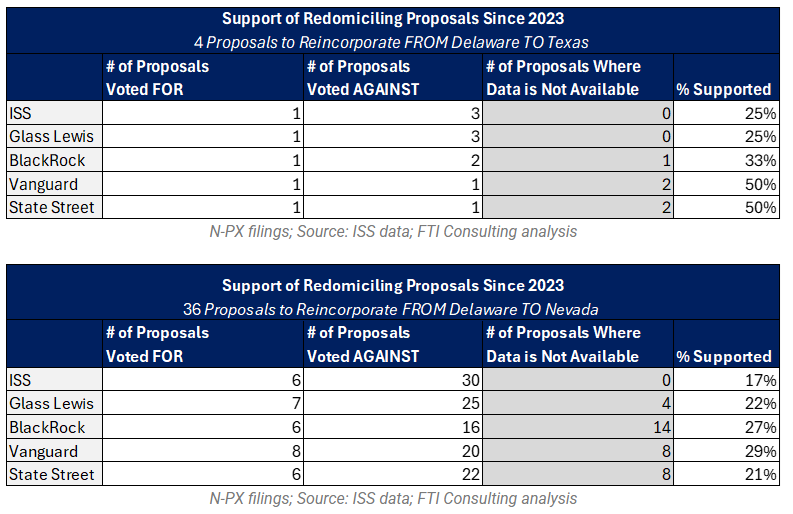

Below is a summary of how ISS, Glass Lewis, and the Big 3 describe their view on reincorporation proposals and how they have voted over the past 3 years:

- ISS Policy: “General Recommendation: Management or shareholder proposals to change a company’s state of incorporation should be evaluated case-by-case, giving consideration to both financial and corporate governance concerns including the following: reasons for reincorporation; comparison of company’s governance practices and provisions prior to and following the reincorporation; and comparison of corporation laws of original state and destination state. Vote for reincorporation when the economic factors outweigh any neutral or negative governance changes.”

- Glass Lewis Policy: “The Benchmark Policy is generally of the view that the board is in the best position to determine the appropriate jurisdiction of incorporation for the company. However, all proposals to reincorporate to a different state or country are reviewed on a case-by-case basis. This review includes the changes in corporate governance provisions, especially those relating to shareholder rights, material differences in corporate statutes and legal precedents, and relevant financial benefits, among other factors, resulting from the change in domicile.”

- BlackRock Stewardship Policy: “We evaluate the economic and strategic rationale behind the company’s proposal to reincorporate on a case-by-case basis. In all instances, we evaluate the changes to shareholder protections under the new charter/articles/bylaws to assess whether the move increases or decreases shareholder protections. Where we find that shareholder protections are diminished, we may support reincorporation if we determine that the overall benefits outweigh the diminished rights.”

- Vanguard Stewardship Policy: “Management proposals to reincorporate to another domicile will be evaluated case by case based on the relative costs and benefits to both the company and shareholders. Considerations include the reasons for the relocation and the differences in regulation, governance, shareholder rights, and potential benefits.”

- State Street Stewardship Policy: Does not state an explicit view for reincorporation but notes “the reorganization of the structure of a company or mergers often involve proposals relating to reincorporation, restructurings, liquidations, and other major changes to the corporation. We expect proposals to be in the best interests of shareholders, demonstrated by enhancing share value or improving the effectiveness of the company’s operations.”

Companies should be mindful of the fact that BlackRock, Vanguard, and State Street all now have two separate stewardship teams – effectively changing the “Big 3” to the “Big 6” and doubling the number of stewardship teams they should engage with. The above summarizes how their traditional stewardship teams approach the topic, not the newly created teams.

We encourage Boards not to make extrapolations based upon support levels and pass/fail outcomes of other companies, particularly given small sample sizes, the difference in companies’ shareholder bases (i.e., controlling shareholders), and that each jurisdiction and company has different sets of factors for shareholders to consider. Any analysis of how a company’s specific shareholders would view redomiciling should be done thoughtfully to account for these factors.

Some investors’ voting policies start with the assumption that economic benefit and shareholder rights may be inherently at odds when reincorporating. Ideally, Boards can articulate that this is not the case. While economic benefit is obviously important to increasing shareholder value, shareholders will also assess shareholder rights and board accountability. This tension between economic profit and board accountability is a founding principle of corporate governance and stewardship teams – boards should not underestimate the importance that shareholders will put on one over the other.

As this topic is put to vote more often, we expect shareholders will start to build a more comprehensive “framework” for evaluating when to support or vote against a DExit proposal. For now, however, the analysis is very much “case-by-case.”

Eight Tactical Considerations for Boards Considering Reincorporation

When Evaluating the Possibility of Reincorporation:

- Candidly Assess Current Relationship With Shareholders. Requesting shareholder approval to reincorporate does not happen in a vacuum. History matters. When shareholders are voting, they will be assessing more than just the merit of the proposal. They will be assessing the history of engagement with the Company, the Company’s current shareholder rights profile, the Board’s rapport with shareholders at large, and, if applicable, any response to previous shareholder dissent. Shareholders need to trust the Board in order to support such a proposal, and trust is established well before the filing of a preliminary proxy.

- Start Early. Companies should thoroughly assess the merit of reincorporation, including to which jurisdictions, alongside legal counsel. Shareholders will want to see that the Board took the appropriate steps to determine this was in the best interest of shareholders, and this process was not rushed. Further, reincorporation requires the filing of a preliminary proxy and a deliberate campaign-like approach to secure shareholder support (more on that below), which underscore the importance of starting early.

- Avoid Surprises (for your shareholders and for you).

- Engage Shareholders Early. Companies should have regular dialogue with their top investors on governance matters, establishing a relationship with them before requesting their support on a proposal like reincorporation. In these engagements, companies can discuss the topic of reincorporation at a high level with their top shareholders and seek their views on the topic.

- Conduct a Voting Outlook. Prior to requesting shareholder approval to reincorporate, a Company should have a rough idea of which shareholders are generally supportive, unsupportive, or “on the fence” when it comes to reincorporation proposals. Analysis can inform a likely vote outcome and can identify what levers the company has available to increase the likelihood of shareholder support.

- Monitor the Landscape. The legal frameworks that may make reincorporation more or less appealing can change over time. We expect shareholders’ views will also evolve. Boards considering reincorporating should closely monitor these developments.

When Seeking Shareholder Approval for Reincorporation

5. Proactively Plan a Campaign. Any Company seeking reincorporation should plan a cohesive campaign to secure shareholder support. Informed by a voting outlook, companies should know what levers are available to secure shareholder support and how to approach optional provisions. A well-run campaign not only has compelling proxy materials and an engagement strategy tailored to each investor but it also has scenario plans for potential hurdles like an adverse recommendation from a proxy advisor, scrutiny from shareholder proponents, or unwanted media coverage.

6. Why You and Why Now. Companies must have a compelling company-specific rationale behind reincorporating that goes beyond “less litigation.”

7. Approaching the Optional Choices. For states like Texas, where there are optional provisions to consider, Boards should seek to understand the perceived tension between economic benefit and shareholder rights. If reincorporation puts shareholders’ rights at risk, the probability of securing shareholder support will decrease. Ideally, Boards can lean on direct shareholder feedback and intel on shareholder preferences from their advisors to inform these decisions.

8. Do Not Hide From The Risks. Shareholders are aware of the risks that come with a DExit move, such as losing the extensive case law available in Delaware. It’d be unrealistic to ignore these risks entirely. Instead, Boards should communicate how they assessed the risks inherent in this move and determined that the benefit to shareholders would outweigh potential risks.

Above all, shareholders and their stewardship teams cast votes based upon what they believe is best for their investment over the long term. DExit proposals are no different. In many cases, that assessment can generally be distilled into assessing the economic benefit to the Company as well as the impact on shareholder rights’ and the Board’s accountability to its shareholders. These may, but do not need to be, at odds with each other.

In the case of reincorporation, shareholders will assess what is best for their investment by balancing factors like litigation costs, business-friendly court systems, legal (un)certainty with court outcomes, shareholder rights, and shareholder engagement. Each company will be assessed based upon their specific factors within these categories.

With how nascent DExit is, any Board pursuing this must thoroughly assess the benefits and risks to reincorporation, which are fluid and will continue to evolve – as will investor views towards reincorporation. Boards seeking reincorporation will need to have a carefully considered plan that is initiated well before the proposal is put to a vote and culminates in a well-run, proactive, campaign to secure shareholder support.

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.